Market Wrap 2026-02-24

- European stock markets decline as concerns about AI impact European banks; US equity futures show a slight recovery.

- The Japanese Yen weakens following reports that PM Takaichi expressed reservations to BoJ Governor Ueda regarding interest rate increases; the Dollar Index (DXY) is slightly stronger.

- UK Gilts reach a new contract high ahead of the Treasury Select Committee (TSC) meeting, while US Treasury notes remain range-bound before a busy schedule of speakers.

- West Texas Intermediate (WTI) and Brent crude oil prices experience modest gains; spot gold price decreases from Monday's high, while copper prices increase as mainland China returns to trading.

- Key events to watch include US ADP employment data, House Prices (Dec), Consumer Confidence (Feb), Dallas and Richmond Fed surveys (Feb), Atlanta Fed GDPNow, NBH Policy Announcement, and speeches from ECB's Lagarde, BoE's Bailey, Greene, Taylor & Pill, and Fed's Goolsbee, Collins, Bostic, Waller, and Cook & Barkin. Also, US supply data and earnings reports from Home Depot and Keurig Dr Pepper are expected.

Newsquawk in 3 steps:

- Subscribe to the free premarket movers reports

- Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news

squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European stock markets are generally weaker (STOXX 600 -0.1%), with the IBEX 35 (-0.7%) underperforming due to the impact of banks. Conversely, the SMI (+0.6%) is showing modest gains.

- European sectors are mostly positive, with Utilities (+1.7%) and Materials (+0.7%) leading, supported by companies like Sika (+1.9%), Givaudan (+2.2%), and Croda (+2.7%). Sika's stock is rising as the board proposes a 2.8% increase in the gross dividend per share. Croda reported its FY25 earnings, with revenue and EBITDA increasing year-over-year, and FY26 guidance aligning with forecasts, boosting the broader chemicals sector. Banks (-1.1%) are declining due to weak Q4 earnings from Standard Chartered (-1.9%) and concerns about the impact of Anthropic's Claude AI on jobs, as it can automate COBOL modernization.

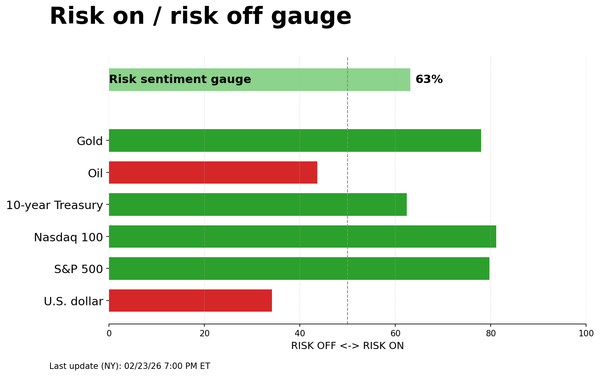

- US equity futures (NQ +0.3%, ES/RTY +0.2%) are showing a modest rebound after Monday's sell-off, influenced by renewed AI concerns. A Citrini report suggested that AI could significantly displace workers, potentially raising unemployment to 10% within 18 months and causing a recession.

- Standard Chartered (STAN LN/2888 HK) reported Q4 2025 adjusted pre-tax profit of USD 1.24 billion (expected USD 1.38 billion), operating revenue of USD 4.85 billion (expected USD 4.91 billion), pre-tax profit of USD 814 million (expected USD 1.1 billion), and net interest income (NII) of USD 3 billion, a 1% year-over-year decrease. FY2025 profit attributable was USD 5.1 billion, a 25.6% year-over-year increase. The company announced an additional USD 1.5 billion share buyback.

- According to Reuters, a senior official from the US President Trump administration stated that Chinese AI startup DeepSeek's latest AI model was trained on NVIDIA's (NVDA) most advanced AI chip, the Blackwell, despite US export controls.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- The Dollar Index (DXY) is slightly firmer, trading around the midpoint of a 97.69-97.95 range, with the day's high slightly above its 50-day moving average (DMA). The main themes in the US are the trade situation and growing concerns about AI, leading to increased uncertainty about the US economy and the USD. However, the index is firmer due to significant pressure on the Japanese Yen (JPY). Focus will be on US Tier 2 data, including Consumer Confidence, the Richmond Fed Index, and the ADP Employment Change Weekly. Fed speakers include Waller, Cook, Barkin, Goolsbee, Bostic, and Collins. US President Trump is scheduled to deliver his State of the Union address, expected to cover the economy, new policies, and potentially trade (02:00 GMT Wednesday / 21:00 EST Tuesday).

- The Japanese Yen (JPY) is weaker, down approximately 0.8%, with USD/JPY trading at the upper end of a 154.52 to 156.27 range, pivoting around its 50 DMA at 155.97. Overnight, pressure arose from reports that US Treasury Secretary Bessent initiated rate checks, rather than at the request of Japan. The JPY's weakness was compounded by reports that PM Takaichi expressed reservations to BoJ Governor Ueda about further rate hikes, reportedly being "stricter than at the previous meeting" in November. Last week, traders had assigned some risk that the PM would ask Ueda to cull future rate hikes during their meeting; despite this, Ueda suggested that the PM "didn't have any particular requests".

- Other G10 currencies are broadly incrementally firmer or flat against the USD. Antipodean currencies are benefiting from positive sentiment in the APAC session and strength in base metals. EUR/USD remains steady within a narrow 1.1767-1.1796 range, with the day's low slightly below its 50 DMA at 1.1772.

FIXED INCOME

- Japanese Government Bonds (JGBs) were boosted by a Mainichi report that PM Takaichi expressed reservations to BoJ Governor Ueda about further tightening, with Takaichi's stance described as "stricter" than at their last meeting. This lifted JGBs by around 30 ticks to a peak of 133.10.

- US Treasury notes (USTs) are flat, trading in a narrow 113-07+ to 113-13 range. Markets are awaiting further updates on the AI disruption narrative, US-Iran relations, and comments from numerous Fed officials. Key speakers include Cook, who supported waiting after December to cut again and described tariff price-rises as temporary in early February, and Waller, who has already spoken post-SCOTUS, saying the impact would likely be limited. The docket also includes Barkin, Goolsbee, and Collins.

- German Bunds are firmer by around 10 ticks, holding just off a 129.73 peak, slightly above Monday's high of 129.71. ECB's Lagarde is scheduled to speak, although she has spoken extensively recently. The benchmark will likely follow leads from USTs and the global risk tone, depending on updates regarding AI, tariffs, or US-Iran relations.

- UK Gilts are also firmer by around 10 ticks, reaching a peak of 92.97, surpassing the January high and reaching a new year-to-date and contract high. The main event for the UK is the Treasury Select Committee, featuring Governor Bailey, dove Taylor, and hawks Greene & Pill. Focus will be on the Governor and the two hawkish members for any indication that recent data or tariff updates have shifted them towards easing in the near term. Commentary will inform the ongoing debate between March and April, with 21bps of easing implied for March and 27bps in April.

- Italy sold EUR 2.5 billion of 2.20% 2028 BTP Short Term (vs. expected EUR 2-2.5 billion) and EUR 2.0 billion of 1.10% 2031, 1.80% 2036 BTPei (vs. expected EUR 1.5-2 billion).

- The UK sold GBP 3 billion of 4.125% 2033 Gilt with a bid-to-cover ratio of 3.37x (previous 3.18x), an average yield of 4.075% (previous 4.296%), and a tail of 0.2bps (previous 0.2bps).

- Japan's Finance Ministry is reportedly considering tweaking liquidity-enhancement auctions and further reducing super-long supply to stabilize yields.

- Australia sold AUD 1.2 billion of 4.25% March 2036 bonds with a bid-to-cover ratio of 2.71 and an average yield of 4.6969%.

COMMODITIES

- Crude oil benchmarks are mostly firmer amid ongoing geopolitical tensions between the US and Iran. WTI and Brent are trading at the upper end of their respective USD 66.16-66.95/bbl and USD 70.87-71.78/bbl ranges.

- Spot gold has declined from Monday's gains, hovering just below USD 5,200/oz, weighed down by recent USD strength. XAU and XAG are trading in the lower ranges of USD 5135.135-5250.005/oz and 84.785-88.756/oz, respectively.

- Copper prices have increased as China returns to the market after the holiday period. The red metal is trading above USD 13,000/t. 3M LME copper is trading in the upper range of USD 13.005-13.061k/t.

- UBS suggests spot gold may reach USD 6,200/oz in the near future due to the factors driving its recent rally.

- The UK is imposing new sanctions on Russia's Transneft oil operation.

- The Shanghai Gold Exchange will cut margin ratios and price limits for some gold and silver contracts from the closing settlement on February 24th.

- Chevron (CVX) has entered exclusive talks to acquire Lukoil's stake in Iraq's West Kerner II oil field (480k bpd) as US sanctions pressure the Russian firm to divest.

- New Zealand will lower the price cap on Russian crude oil.

TRADE/TARIFFS

- US President Trump's 10% global tariff rate takes effect.

- China's Commerce Ministry called on the US to abandon unilateral tariffs, stating it will adjust countermeasures and monitor US actions, and is willing to hold a 6th round of trade talks with the US.

- China's MOFCOM is adding 20 Japanese companies, including Mitsubishi Heavy Industries, to its export control list for military activities, banning exports of dual-use items, and will add another 20 groups to a watch list.

- The EU warns the US that President Trump's new tariff policy violates the trade agreement.

- Japan's finance minister Katayama said they will closely examine details of the US Supreme Court decision on tariffs, will steadily carry out the US-bound investment package, and must be aware that US tariffs on cars remain in effect.

- Japan's Trade Minister Akazawa held a phone conversation with US Commerce Secretary Lutnick on Monday, and both sides affirmed investment plans.

- According to Bloomberg, US President Trump's administration is likely to face tough legal obstacles if it opposes refunds for the tariffs struck down by the US Supreme Court.

- According to the WSJ, US President Trump is reportedly considering new national security tariffs after the SCOTUS ruling, with new levies on a half-dozen industries issued separately from the new global 15% flat-rate tariff.

- Taiwan's Vice Premier said preferential terms reached with the US under the tariff and trade deal would not change, and they will have proactive talks with the US to ensure their interests are protected under deals already reached with Washington.

- China announces that the hot-rolled steel coil issue with South Korea has been resolved.

NOTABLE EUROPEAN DATA RECAP

- French Business Climate Indicator (Feb) 97 (Previous 99).

- French Business Confidence (Feb) 102 vs. Expected 104 (Previous 105).

CENTRAL BANKS

- According to Mainichi citing sources, Japanese PM Takaichi reportedly relayed to BoJ Governor Ueda her reservations about further rate hikes.

- Chinese Loan Prime Rate 1Y (Feb) 3.00% vs. Expected 3.00% (Previous 3.00%).

- Chinese Loan Prime Rate 5Y (Feb) 3.50% vs. Expected 3.50% (Previous 3.50%).

- NBP's Glapinski said monetary policy needs to be cautious.

NOTABLE US HEADLINES

- According to the WSJ, US President Trump will use the State of the Union address to sell the public on the economy and unveil new measures to lower costs ahead of the mid-terms.

GEOPOLITICS

RUSSIA-UKRAINE

- Russia's Kremlin highlights that the special operation goals have not yet been achieved and cannot provide a date for the next round of Ukraine talks.

- The Russian Foreign Ministry Spokesperson said Russia will seek to find a solution to the problem of NATO's expansion to its borders by military or political means, adding that without solving the problem of NATO's expansion to Russia's borders, it is impossible to solve the situation in Ukraine.

- Ukrainian President Zelensky said they will do everything necessary to ensure a strong and lasting peace.

MIDDLE EAST

- According to sources, Iran reportedly nears a deal to purchase anti-ship missiles from China.

- An Israeli official tells Yedioth Ahronoth that a US attack on Iran is imminent.

- According to the NYT, US President Trump said top general Dan Caine predicts an easy victory over Iran, which is in contrast to recent comments by Caine.

- According to CBS News, US President Trump is growing frustrated by the limited military options against Iran, with advisers warning that strikes may not be decisive and risk escalating the conflict.

- US President Trump on Truth said "If we don't make a deal, it will be a very bad day for Iran".

OTHERS

- China said it is open to nuclear talks in Geneva and urges the US to resume strategic stability dialogue with Russia.

- According to SCMP, South Korea and the US are reportedly at odds over war games’ scale, with the US pushing back on South Korea's request for smaller drills, forcing the postponement of a major joint military briefing.

CRYPTO

- Bitcoin slips to USD 63,000, while Ethereum falls further below USD 2,000.

APAC TRADE

- APAC stocks traded with a mostly positive bias as key participants returned to the market and with the region attempting to shrug off the weak lead from Wall St, where sentiment was weighed on by trade uncertainty and AI disruption concerns.

- The ASX 200 struggled for direction as outperformance in the mining, energy and resources sectors was offset by losses in tech, real estate and financials, while participants continued to digest a slew of earnings.

- The Nikkei 225 rallied back above the 57,000 level on return from the long weekend, but is off today's best levels amid losses in tech stocks and after China's MOFCOM added 20 Japanese companies to its export control list, which bans Chinese exports of dual-use items.

- The Hang Seng and Shanghai Comp were mixed, with the mainland boosted on return from a 10-day closure and got the first opportunity to react to the recent US tariff developments, which are seen to benefit China the most, while the Hong Kong benchmark underperformed in a reversal of the prior day's rally amid notable losses in tech and pharmaceuticals.

NOTABLE APAC HEADLINES

- According to Nikkei, several senior US officials said the “rate checks” carried out when the yen weakened in January were initiated by US Treasury Secretary Bessent rather than at Japan’s request. US officials indicated that coordinated intervention to buy yen and sell dollars would have been considered if requested by Japan.

- According to the Wall Street Journal, Japanese Finance Minister Katayama said Japan is keeping close dialogue with the US on Forex.

More

markets stories on ZeroHedge