Market Wrap 2026-02-25

Today's US Market Wrap — Key Points

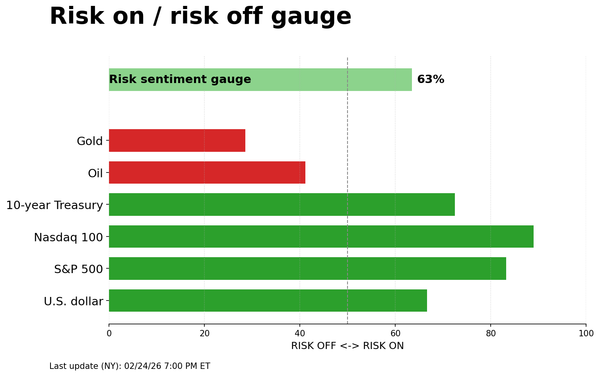

- Equities fell amid AI disruption & tariff concerns, driving risk-off sentiment.

- Focus shifts to central bank speakers & upcoming economic data releases.

- Geopolitical tensions & US/Iran talks remain key market drivers.

- NVDA earnings are a focal point this week.

Already a member? Sign in to unlock the full wrap

MARKET OVERVIEW

- SNAPSHOT: Equities declined, Treasuries advanced, Crude oil decreased, the Dollar showed mixed performance, and Gold increased.

- PREVIOUS SESSION: A research firm highlighted concerns about potential AI disruption; President Trump increased Section 122 tariffs from 10% to 15% and suggested the possibility of even higher tariffs; the EU Parliament postponed a vote on an EU-US trade agreement; Fed Governor Waller indicated that a March rate decision is uncertain; Witkoff and Kushner are scheduled to meet with Iran on Thursday; the Pentagon is urging President Trump to pursue a diplomatic approach; US Secretary of State Rubio's visit to Israel was rescheduled from the weekend to Monday; Hungary reportedly intends to block EU decisions regarding Ukraine until the Druzhba pipeline flow resumes; Novo Nordisk's CargriSema trial results were disappointing; and PayPal is reportedly attracting takeover interest.

- UPCOMING: Data releases include US ADP Weekly data, House Prices (December), Consumer Confidence (February), Dallas/Richmond Fed surveys (February), and Atlanta Fed GDP estimates. Events include the PBoC LPR announcement and the NBH Policy Announcement. Speakers include the BoE's Lombardelli, Bailey, Greene, Taylor, and Pill; the Fed's Goolsbee, Collins, Bostic, Waller, Cook, and Barkin; and the ECB's Lagarde. Supply announcements are expected from Australia, the UK, Italy, and the US. Earnings reports are due from Home Depot, Standard Chartered, and Keurig Dr Pepper.

- WEEK AHEAD: Key events include NVDA earnings, Australian CPI, Tokyo CPI, PBoC LPR, and BoK meetings.

- CENTRAL BANK WEEKLY: A preview of the PBoC LPR and BoK meetings, and a review of the RBNZ, FOMC Minutes, RBA Minutes, and reports on the ECB President Job.

- WEEKLY US EARNINGS ESTIMATES: Tech company NVDA is a focal point.

MARKET WRAP

Monday's session was characterized by risk aversion, with equities falling due to concerns about further AI disruption and President Trump's tariff increases. The AI concerns stemmed from research suggesting significant downside risks if AI surpasses expectations. While not the firm's base case, the research indicated a potential unemployment spike to 10% and a 38% decline in the SPX from projected late-2026 peaks (estimated at 8,000), along with a recession in 2027. The report identified payments, software, and private credit stocks as particularly vulnerable. These sectors experienced declines on Monday, and IBM also suffered a significant loss following Anthropic's announcement that Claude can now automate COBOL modernization efforts, further fueling AI disruption fears. On the trade front, President Trump raised Section 122 tariffs to 15% from 10% over the weekend. Mexico announced that it would pay reduced tariffs on non-USMCA-compliant goods, while the EU has suspended trade talks with the US and is not seeking to modify the existing agreement at this time. President Trump warned that countries engaging in "games" would face higher tariffs than recently agreed upon. The risk-off sentiment driven by AI disruption and tariff increases led to increased demand for T-notes throughout the US session, with prices settling near their highs. Attention is now shifting to supply in a week with limited data releases. However, several central bank speakers are scheduled for Tuesday. Governor Waller spoke today, stating that a rate cut or hold in March is almost equally likely. In FX markets, the Dollar's performance was mixed against other currencies, while activity currencies underperformed in the risk-off environment. Crude oil prices ultimately settled slightly lower, and focus is turning to US/Iran talks on Thursday. Reports indicate that the Pentagon has been urging President Trump to pursue a diplomatic resolution, citing the risks of striking Iran. President Trump has reportedly been considering strikes but has agreed to allow Witkoff and Kushner more time to negotiate a diplomatic solution. Gold and Silver prices increased due to the risk-averse conditions, while Bitcoin declined.

US

FED GOVERNOR WALLER (VOTER):

- Governor Waller stated that he would support a 25bps rate cut in March if January's strong labor market data is revised downward or disappears, but it may be appropriate to hold rates steady if downside risks to the labor market have diminished. Regarding the March meeting, he views the two possible outcomes as nearly equally likely and stated that he needs to see the February jobs report due March 6 before making a judgment on a labor market rebound. Following the SCOTUS decision to strike down President Trump's IEEPA tariffs on Friday, Governor Waller said it may have a positive impact on spending and investment, will look through tariffs if they come down, and added that the ruling is unlikely to have a significant impact on his view of the appropriate policy stance. Looking ahead, he estimates January PCE inflation of approximately 2.8% over the next 12 months, with core inflation at around 3%, but believes underlying inflation without tariff effects is close to 2%. Governor Waller expects real GDP to grow above 2% over the next six months after accounting for shutdown effects. He noted that there are reasons, including AI, to believe that hiring may remain weak, and said a weak labor market is likely to continue going forward.

FIXED INCOME

T-NOTE FUTURES (H6) SETTLED 14 TICKS HIGHER AT 113-12

T-notes experienced increased demand as President Trump raised tariffs and sentiment was negatively affected by concerns about further AI disruption. At settlement, the 2-year yield decreased by 4.2bps to 3.438%, the 3-year yield decreased by 5.7bps to 3.444%, the 5-year yield decreased by 6.9bps to 3.579%, the 7-year yield decreased by 6.8bps to 3.780%, the 10-year yield decreased by 6.0bps to 4.025%, the 20-year yield decreased by 4.1bps to 4.632%, and the 30-year yield decreased by 3.1bps to 4.694%.

THE DAY:

T-notes increased on Monday, partially reversing the declines following the IEEPA decision, as President Trump increased Section 122 tariffs to 15% from 10%, which is expected to increase government revenues. The increase began overnight and continued throughout the European session, but the increase accelerated during the US session. There were no tier 1 data releases to analyze, but there was significant focus on further AI disruption, which negatively affected sentiment and supported T-notes through haven demand. T-notes reached a high of 113-14 from overnight lows of 112-27+. Fed Governor Waller spoke at NABE, where he said the decision for March is close to a coin flip between a cut and a hold. He is largely data dependent, noting if labor market data for February is consistent with stronger job creation and low unemployment, it may be appropriate to hold, but if the good labor market news in January is revised away, or evaporates in February, he would support a 25bps cut in March. He stressed the decision hinges on the February labor and inflation data.

SUPPLY

Bills

- The US sold 3-month bills at a high rate of 3.590%, with a bid-to-cover ratio of 3.30x; it sold USD 6-month bills at 3.525%, with a bid-to-cover ratio of 3.03x.

- The US will sell USD 90bln of 6-week bills on February 24th; all to settle February 26th.

Notes

- The US will sell USD 69bln of 2-year notes on February 24th, USD 70bln of 5-year notes on February 25th, and USD 44bln of 7-year notes on February 26th; all to settle March 2nd.

- The US will sell USD 28bln of 2-year FRN's on February 25th; to settle February 27th.

STIRS/OPERATIONS

- Market Implied Fed Rate Cut Pricing: March 0bps (previous 0bps), April 3.2bps (previous 3.2bps), June 13.6bps (previous 12.5bps), December 57.3bps (previous 53.9bps).

- SOFR at 3.66% (previous 3.67%), volumes at USD 3.224tln (previous USD 3.238tln) on February 20th.

- EFFR at 3.64% (previous 3.64%), volumes at USD 101bln (previous USD 100bln) on February 20th.

- NY Fed RRP op demand at USD 0.88bln (previous 0.5bln), across 7 counterparties (previous 4) on February 23rd.

CRUDE

WTI (J6) SETTLED USD 0.17 LOWER AT 66.31/BBL; BRENT (J6) SETTLED USD 0.27 LOWER AT 71.49/BBL

The crude oil complex began the week with losses, albeit in a volatile session, as participants continued to assess geopolitical relations. The latest information on US and Iran is that the Pentagon's General Caine (Joint Chief Chairman) is raising concerns to President Trump about an extended military campaign against Iran, advising that war plans being considered carry risks including US and Allied casualties, depleted air defenses and an overtaxed force. President Trump is said to have been leaning towards launching a strike for several days, but agreed to give Witkoff and Kushner more time for negotiations. In terms of meetings, US Secretary of State Rubio postponed his Saturday visit to Israel, now scheduled for next Monday, while Witkoff and Kushner are to meet with Iran in Geneva on Thursday. Elsewhere, news flow was sparse on Monday in a week with a lack of tier 1 US data, as traders await any geopolitical developments, Fed speak, and/or Nvidia earnings on Wednesday. For the record, WTI traded between USD 65.38-67.28/bbl and Brent USD 70.28-72.04/bbl.

EQUITIES

CLOSES: SPX -1.04% at 6,838, NDX -1.21% at 24,709, DJI -1.66% at 48,804, RUT -1.61% at 2621

SECTORS: Materials +2.04%, Health +1.96%, Industrials +1.38%, Consumer Discretionary +0.94%, Technology +0.66%, Real Estate +0.62%, Utilities +0.49%, Financials +0.45%, Consumer Staples +0.13%, Communication Services -0.49%, Energy -2.81%

EUROPEAN CLOSES: Euro Stoxx 50 -0.24% at 6,117, Dax 40 -1.09% at 24,987, FTSE 100 -0.02% at 10,685, CAC 40 -0.22% at 8,497, FTSE MIB +0.49% at 46,699, IBEX 35 +0.57% at 18,290, PSI +1.71% at 9,246, SMI +0.21% at 13,866, AEX -0.12% at 1,016

STOCK SPECIFICS:

- Alphabet (GOOGL) was upgraded at Wells Fargo to 'Overweight' from 'Equal Weight'.

- Arcellx (ACLX) is to be acquired by GILD for $7.8bln or $115/shr; ACLX closed Friday at 64.11.

- Domino’s Pizza (DPZ) reported a revenue beat and a 15% increase in its quarterly dividend.

- General Mills (GIS) was downgraded at BofA to 'Neutral' from 'Buy'.

- Getty Images (GETY) and Shutterstock (SSTK) received unconditional US antitrust clearance from the DoJ for their merger.

- Novo Nordisk’s (NVO) CagriSema 2.4 did not meet the primary endpoint of showing non-inferiority on weight loss vs. Eli Lilly’s (LLY) tirzepatide 15mg at 84 weeks.

- Nvidia (NVDA) laptop chips are set to launch this year in products from Dell (DELL) & Lenovo (LNVGY).

- President Trump said Netflix (NFLX) should fire Susan Rice “immediately” or “pay the consequences”.

- V.F. Corp (VFC) was downgraded at JPM to 'Underweight' from 'Neutral'.

- Veris Residential (VRE) is to be acquired by Affinius for $3.4bln or $19/shr; VRE closed Friday at 16.77.

- Abbott (ABT) reportedly seeks USD 20bln in US bond sales for Exact Science (EXAS) deal.

- PayPal (PYPL) is said to be attracting takeover interest after a share slump; the company has filed bank meetings amid unsolicited interest; suitors are showing early interest for all or part of the company. PayPal interest is preliminary and may not lead to any deals.

- IBM (IBM) declined following an update from Anthropic stating that Claude code can now automate COBOL modernization efforts.

FX

The Dollar Index was relatively flat to begin the week, showing mixed performance against G10 currencies, as participants considered the latest tariff updates and comments from Fed Governor Waller. Regarding tariffs, President Trump increased the blanket tariff rate to 15% from 10% over the weekend, and later added that any country that wants to "play games" with the SCOTUS decision, especially those who ripped off the US, will be met with a much higher tariff, and worse, than what they recently agreed to. On Fed speak, Governor Waller sees the March FOMC decision as a “coin-flip” and noted it will all depend on the February jobs and inflation data. Overall, headline news flow was rather light to start the week ahead of a plethora of Fed speakers on Tuesday, Nvidia earnings on Wednesday, and the ever present focus on geopolitical tensions, tariff updates and AI.

JPY was the G10's strongest performer, seemingly supported by the risk-off sentiment seen throughout the session as AI concerns resurfaced, weighing on software names and IBM, with the latter impacted by a separate update.

GBP, EUR, and CHF all experienced slight strength against the Greenback. In Europe, the German Ifo was better than expected. In the tariff space, European MP Lange said they have decided to postpone the vote on a US trade deal, which was set for Tuesday and intend to vote eventually, but they need clarity first. That followed earlier reports that the EU is set to freeze trade deal approval over US President Trump's tariff risk. ECB President Lagarde remarked that inflation and policy are in a good place; ECB will decide policy meeting-by-meeting, must remain agile, and completing the term is her baseline. For the Pound, BoE's Taylor said they are 2-3 cuts away from neutral.

Antipodeans and the Loonie underperformed and weakened against the Dollar as risk sentiment weighed, as opposed to any currency-specific developments. On the Aussie, SocGen notes that a very large (and growing) net AUD long position makes January CPI data important, which is due early Wednesday morning GMT. The market expects a steady trimmed mean rate at 3.3% Y/Y, with eyes on RBA Governor Bullock speaking at a ‘Fireside Chat’ later that morning (UK time).