Market Wrap 2026-02-27

MARKET UPDATE

- During the third round of nuclear discussions in Geneva, the Foreign Minister of Oman stated that Iran and the United States have responded positively to proposals, and negotiations are ongoing. Al Jazeera reported that the "Iranian negotiating delegation meets IAEA director at the headquarters of the negotiations in Geneva."

- European equity markets are mixed. US equity futures are struggling to advance despite NVIDIA's earnings report (+0.8% pre-market).

- The DXY is showing modest gains, while the JPY is outperforming due to hawkish comments. The GBP is weaker ahead of the Gorton and Denton by-election.

- Global fixed income benchmarks are stable as markets await data, supply announcements, and remarks from the Federal Reserve.

- Crude oil benchmarks are declining following positive statements from the Omani Foreign Minister, which could potentially de-escalate tensions.

- Upcoming highlights include US Jobless Claims, Japanese Tokyo CPI (Feb), and Retail Sales (Jan). Speakers include Fed officials Bowman, Miran, and Goolsbee. Supply announcements are expected from the US. Earnings reports are due from CoreWeave, Intuit, Vistra Energy, Autodesk, Dell, and Warner Bros Discovery.

EUROPEAN TRADE

EQUITIES

- European stock exchanges (STOXX 600 +0.1%) are displaying mixed performance, with the CAC 40 in France (+0.4%) leading gains and the IBEX 35 in Spain (-0.3%) lagging.

- There is no clear bias among European sectors. Financial Services (+1.3%) and Retail (+1.0%) are the top-performing sectors, while Basic Resources (-2.0%) are underperforming due to falling silver prices. LSEG (+6.7%) is supporting the Financial sector, having announced a new GBP 3 billion share buyback program. In the Retail sector, Howden Joinery (+7.5%) released a positive FY report, showing an annual increase in pretax profit. The company's share price increase is attributed to the announcement of a GBP 100 million share buyback.

- US equity futures (NQ -0.1%, ES/RTY U/C) are flat to slightly weaker, despite a positive Q4 earnings report from Nvidia. Goldman Sachs analysts released a note following the earnings, reiterating a Buy rating on the stock and stating that they see a clearer path to stock outperformance. However, HSBC lowered its price target to USD 295 per share from USD 310.

- Rolls Royce (RR/ LN) FY 2025 (GBP): Revenue 20.05 billion (previous 17.84 billion Y/Y), Operating Profit 3.46 billion (previous 2.46 billion Y/Y), Basic EPS 29.55 (previous 20.29 Y/Y). The company announced a multi-year share buyback program of GBP 7 billion - 9 billion.

- NVIDIA Corporation (NVDA) Q4 2026 (USD): Adjusted EPS 1.62 (expected 1.54), Revenue 68.1 billion (expected 66.12 billion). The company projects Q1 revenue between USD 76.44-79.56 billion (expected 72.6 billion), excluding any data center revenue from China, although it has received licenses to ship small volumes of H200 chips to Chinese customers. Reports indicate that traders were underwhelmed by a routine beat, and there are concerns about customer concentration and competition, while its outlook excluded China data center revenue. NVIDIA shares are up +0.8% pre-market.

- NVIDIA (NVDA) has confirmed that it was granted a US license in February to ship a small amount of H200 chips to China-based customers, and H200 chips face 25% tariffs. Negotiations regarding the OpenAI investment are still ongoing, and the deal is not finalized.

- Baidu (BIDU / 9888 HK) Q4 2025 (USD): Revenue 4.68 billion (expected 4.68 billion), Adjusted EPS 1.52 (expected 1.47).

- Sony (6758 JT) is expanding its share buyback by JPY 100 billion to a total of up to JPY 250 billion.

FX

- The DXY is slightly firmer after finding support around the 97.50 level overnight, attempting to recover some of yesterday's losses. Macro news flow is light as US-Iran nuclear talks begin. The Omani Foreign Minister stated that Iran and the US have welcomed proposals in the Geneva talks. On the data front, the Chicago Fed will release its labor market indicators; weekly jobless claims are expected at 215k from 206k; continuing claims (which coincide with the traditional BLS survey window for the February jobs report) are expected at 1.86 million from 1.869 million. The DXY is currently trading within a 97.49-97.72 range, compared to Wednesday's 97.62-98.00 range.

- The JPY is currently outperforming, as USD/JPY continued to pull back overnight after climbing to its highest levels in over two weeks on Wednesday, following the Takaichi government's reflationist picks for the BoJ board. The pair was affected by the lack of fresh drivers and the absence of tier-1 data from Japan. Comments from BoJ Governor Ueda reiterated the hiking bias, and hawkish dissenter Takata also stated that further rate hikes must be conducted gradually.

- The GBP is taking a breather after advancing in tandem with high-beta FX. News flow for the UK has been light, with price action reflecting a subdued/cautious tone. UK focus will likely be on the Gorton and Denton by-election: analysts suggest that a heavy defeat for the ruling Labour Party could trigger volatility in Sterling. Some suggest a loss in what has been a safe Labour seat for nearly 100 years could reignite speculation regarding UK PM Starmer's leadership.

- Antipodean currencies are subdued following recent outperformance facilitated by their high-beta statuses. Overnight, quarterly capex data from Australia exceeded forecasts, which will factor into next week's GDP release.

FIXED INCOME

- USTs are flat, holding within a 113-04+ to 113-09 range. There is little driving US paper this morning, reflected in the lackluster price action. Wednesday's after-market release of stronger-than-expected NVIDIA earnings had little follow-through from a sentiment perspective. On the data front, the Chicago Fed will release its labor market indicators; weekly jobless claims are expected at 215k from 206k; continuing claims (which coincide with the traditional BLS survey window for the Feb jobs report) are expected at 1.86 million from 1.869 million. From a geopolitical perspective, US-Iran talks have reportedly begun in Geneva. A breakdown in talks could spur some haven inflows in USTs, given the increased likelihood of a US strike on Iran.

- Bunds are following the sideways action of global peers, holding within a 129.57 to 129.69 range. There is a lack of catalysts for German paper this morning, and commentary from ECB President Lagarde also failed to spur action. She reiterated the usual data-dependent and meeting-by-meeting approach.

- Gilts are mirroring peers, currently flat and within a narrow 92.82-92.90 range. Markets were expecting remarks from BoE’s Lombardelli, though nothing has been released thus far. UK focus will likely be on the Gorton and Denton by-election, with some analysts suggesting that a Labour loss, in what has been a safe seat for nearly 100 years, could reignite speculation regarding UK PM Starmer's leadership. This could weigh on Gilts in the short-term.

- Italy sold EUR 6.5 billion (vs. expected EUR 5.5-6.5 billion) of 2.85% 2031 and 3.45% 2036 BTP, and EUR 2.5 billion (vs. expected EUR 2.0-2.5 billion) of 1.468% 2035 CCTeu.

- Abu Dhabi is set to issue two benchmark USD bonds, according to Bloomberg. The 5-year note is offered at a spread of +50bps over USTs, and the 10-year note is offered at a spread of +55bps over USTs.

- UK government debt sales are anticipated to decline for the first time in four years, as large banks forecast GBP 247 billion of gilt issuances in the approaching fiscal year amid Chancellor Reeves' efforts to rein in borrowing, according to the FT.

- Australia sold AUD 150 million in 2030 indexed bonds, with a bid-to-cover ratio of 4.21 and an average yield of 1.8002%.

COMMODITIES

- Crude benchmarks traded lower on the commencement of the US-Iran talks in Geneva. As updates from that meeting were announced, WTI and Brent dipped to fresh session lows and now trade off by around 1.5% and 1.3% respectively. Two main takeaways from the meeting include the Omani Foreign Minister suggesting that Iran and the US have welcomed proposals in the Geneva talks. Elsewhere, Al Jazeera reported that the “Iranian negotiating delegation meets IAEA director” – this would be necessary for a market-friendly sustainable deal. Brent May’26 is now shy of USD 70.00/bbl, with the low currently a moving a target at the time of writing.

- Precious metals are trading mixed this morning, with spot gold trading firmer and silver lower. XAU and XAG trades within a narrow range of USD 5155.59-5205.58/oz and USD 86.33-90.34/oz, respectively.

- Base metals are lower this morning, tracking headwinds from its largest buyer, China, which saw mixed to weak sentiment, pinning down price action for base metals. Sentiment in Europe has done little to shake off sentiment in the base metal complex, with European equities trading mixed this morning. 3M LME copper trades within the lower range of USD 13.23-13.35k/t.

- Nordic countries are investigating a threat to the region's energy infrastructure, according to TV4 citing sources. An informant stated, “According to the threat, the actor may strike in the near future.”

TRADE/TARIFFS

- German Chancellor Merz, regarding his conversation with Chinese President Xi, said there are many challenges to overcome; the Economic Minister will conduct a follow-up visit.

- India's Trade Minister, after hosting US Commerce Secretary Lutnick, said both parties engaged in "very fruitful" discussions to expand trade and economic partnership.

NOTABLE EUROPEAN DATA RECAP

- EU Consumer Confidence Final (Feb): -12.2 vs. Expected -12.2 (Previous -12.4).

- EU Consumer Inflation Expectations (Feb): 25.8 (Previous 24.2, Revised From 24.1).

- EU Economic Sentiment (Feb): 98.3 vs. Expected 99.8 (Previous 99.3, Revised From 99.4, Low 98.5, High 100).

- EU Selling Price Expectations (Feb): 11.5 (Previous 10.0).

- EU Services Sentiment (Feb): 5.0 vs. Expected 7.5 (Previous 7.2, Low 6.8, High 7.9).

- Italian Consumer Confidence (Feb): 97.4 vs. Expected 97.2 (Previous 96.8).

- Italian Business Confidence (Feb): 88.5 (Previous 89.2).

- Swiss Non-Farm Payrolls (Q4): 5.544 (Previous 5.532).

- Swedish Consumer Confidence (Feb): 96.3 (Previous 95.3).

CENTRAL BANKS

- ECB's Lagarde stated that they continue to expect inflation to stabilize at the 2% target in the medium term and will continue to follow a data-dependent and meeting-by-meeting approach.

- BoJ's Governor Ueda said the basic stance is to continue hiking interest rates if the likelihood of economic and price forecasts materializing heightens, according to Yomiuri. Underlying inflation has not yet fully reached 2%, and policy will be guided to get underlying inflation to around 2%, while avoiding it exceeding 2% on a sustained basis.

- BoJ's Takata said there is no preset pace for rate hikes, and future moves depend on the economic environment and data.

- BoJ Board Member Takata said fears of Japan's economy returning to deflation have been dispelled and believes it's necessary to move the BoJ's focus more to the upswing in prices. He proposed a rate hike in January, viewing that the BoJ must continue adjusting real interest rates, which remain significantly lower than the rates seen overseas.

- The Bank of Korea kept its base rate unchanged at 2.50%, as expected. It raised its 2026 GDP growth forecast to 2.0% from 1.8% and sees 2027 growth at 1.8%. It also raised its 2026 CPI forecast to 2.2% from 2.1% and sees 2027 CPI at 2%.

- The BoK said the rate decision was unanimous, and median projections show the base rate is seen at 2.5% in six months. The Bank will make policy decisions supporting a recovery in economic growth. Growth momentum is expected to remain favorable, with strong chip exports supporting growth.

- BoK Governor Rhee said no board member expects rates to be increased in three months' time and noted that the US tariff ruling is expected to have a limited impact on exports for now.

GEOPOLITICS

MIDDLE EAST

- The Omani Foreign Minister says Iran and the US have welcomed proposals in the Geneva talks.

- Al Jazeera reported that the "Iranian negotiating delegation meets IAEA director at the headquarters of the negotiations in Geneva."

- An Omani mediator in Geneva said that the US and Iran are open to new and creative ideas, according to AFP.

- Iran's Foreign Ministry spokesperson said the country will move to the nuclear negotiation site in half an hour, and the negotiating team has a reasonable amount of flexibility in the US nuclear talks in Geneva.

- Journalist Kais reported that "in Iran, the Omani foreign minister, who is in Geneva, conveyed to the American side the Iranian proposal for an agreement."

- White House officials reportedly argue it would be best if Israel makes the first move regarding striking Iran, according to POLITICO.

- US Secretary of State Rubio said Iran poses a grave threat and seeks nuclear capability, adding that talks on Thursday will focus on the nuclear program and that Iran also poses a conventional weapons threat designed to target the US.

- US VP Vance said they see evidence that Iran is trying to build a nuclear weapon.

RUSSIA-UKRAINE

- The Russian Foreign Minister says they do not have a deadline for reaching a Ukraine settlement but confirms they are working to resolve them.

OTHERS

- South Korea's presidential office states it will continue working towards peaceful coexistence with North Korea, according to News1.

- US Secretary of State Rubio said the US will investigate a deadly speedboat shooting off Cuba after the Cuban Interior Ministry reported its forces killed four people who allegedly opened fire from a Florida-tagged vessel.

CRYPTO

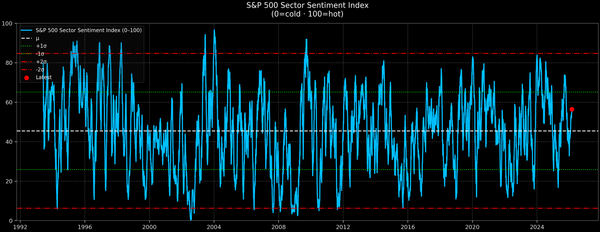

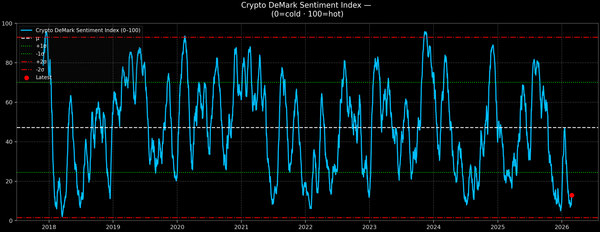

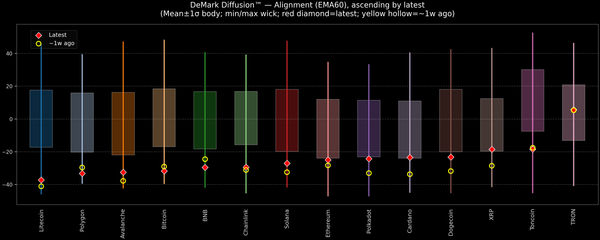

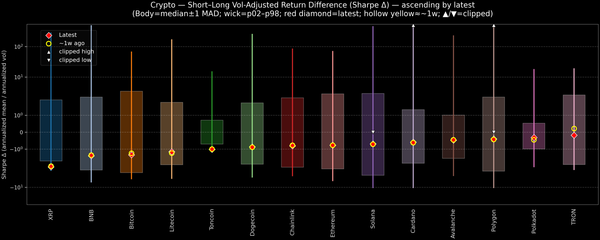

- Bitcoin holds above USD 68,000, while Ethereum regains the USD 2,000 handle.

APAC TRADE

- APAC stocks are mostly positive, with the majority of the region taking its cue from gains on Wall Street, where tech led the advances and NVIDIA posted stronger-than-expected earnings after hours.

- The ASX 200 mildly gained as the outperformance in tech, telecoms, and healthcare offset the losses in energy and industrials, while better-than-expected private capex data also provided some encouragement.

- The Nikkei 225 initially rallied to a fresh all-time high north of the 59,000 level but then pulled back from record levels as the yen gradually strengthened and after BoJ hawkish dissenter Takata called for gradually hiking rates.

- The Hang Seng and Shanghai Comp were ultimately mixed, with the Hong Kong benchmark the laggard amid weakness in tech, consumer discretionary, and insurers, while the mainland was indecisive as price action was contained with very little in the way of fresh catalysts.

NOTABLE APAC DATA RECAP

- Japanese Coincident Index Final (Dec): 114.3 (Previous 114.9).

- Japanese Leading Economic Index Final (Dec): 111 vs. Expected 110.2 (Previous 109.9).

- Australian Private Capital Expenditure for 2025-26 (AUD)(Estimate 5): 199.3B (Previous 191.3B).

- Australian Private Capital Expenditure for 2026-27 (AUD)(Estimate 1): 158.4B.

- Australian Private Capital Expenditure QoQ (Q4) Q/Q: 0.4% vs. Expected 0.0% (Previous 6.4%).

- New Zealand ANZ Activity Outlook (Feb): 52.6 (Previous 51.6).

- New Zealand ANZ Business Confidence (Feb): 59.2 (Previous 64.1).