Market Wrap 2026-03-02

Today's US Market Wrap — Key Points

- Stocks fell amid credit & geopolitical risks, recovering slightly late.

- Treasuries rose on safe-haven demand & reduced Fed rate cut bets.

- Crude oil surged due to US/Iran tensions and potential action.

- PPI exceeded expectations, but inflation fears remained contained.

- Focus shifts to upcoming US payrolls and geopolitical events.

Already a member? Sign in to unlock the full wrap

MARKET SNAPSHOT

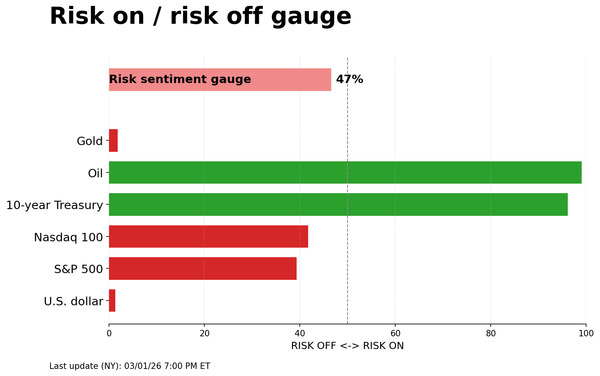

- Equities decreased, Treasuries increased, Crude increased, Dollar decreased, Gold increased.

MARKET RECAP

- Trump stated he is undecided on Iran and is not pleased with their negotiation tactics; US Core and Headline PPI data were higher than anticipated; French and Spanish Preliminary CPI figures were hotter than expected, while German State CPI data were softer; PBoC will reduce the FX Risk Reserve Ratio for forward FX sales; NFLX withdrew from the WBD deal, PSKY prevailed.

UPCOMING EVENTS

- Data releases: German Retail Sales (Jan), EZ/UK/US Final Manufacturing PMIs (Feb), US ISM Manufacturing PMI (Feb), Chinese RatingDog Manufacturing PMI (Feb), Japanese Unemployment Rate (Jan).

- Speeches: BoJ's Himino; BoE’s Taylor, Ramsden; BoC’s Kozicki, Macklem.

- Earnings: Riot Platforms, Norwegian Cruise Line, ASM International.

WEEK AHEAD

- Key events include US NFP, Retail Sales, ISM PMIs, OPEC meeting, EZ Flash HICP, ECB Minutes, and Australian GDP.

CENTRAL BANK WEEKLY

- Preview of ECB Minutes; Review of PBoC LPR and BoK decisions.

WEEKLY US EARNINGS ESTIMATES

- Earnings season is slowing down, with key reports expected from TGT, CRWD, AVGO, and COST.

MARKET WRAP

US stock indices declined on Friday, influenced by credit risk and geopolitical tensions, but reduced losses near the close, moving up from earlier lows. Sector performance was mixed, with Financials underperforming due to ongoing concerns about private credit following the MFS collapse, which affected several US financial institutions, including Wells Fargo, Apollo, and Jefferies. These concerns may be driving a shift from corporate credit to safer government debt, supporting US Treasuries, which rose across the curve as expectations for Fed rate cuts in 2026 diminished. Energy was the top-performing sector, boosted by gains in WTI and Brent crude amid persistent US/Iran tensions and rising concerns about potential US action against Iran. Following discussions, Oman and Iran reported positive talks, but Trump stated he has not decided on Iran and is dissatisfied with their negotiation methods. In the FX market, the Swiss franc outperformed due to safe-haven demand, along with higher gold prices, while the Yen's gains were limited, possibly due to recent BoJ board nominations seen as favoring looser short-term policy. US PPI data exceeded expectations, but inflation fears did not intensify, possibly due to softer PCE components within the report. Market participants will monitor geopolitical developments ahead of the US payrolls report next Friday.

US

PPI:

- Both headline and core PPI metrics exceeded expectations in January. The headline M/M increased by 0.5%, surpassing the 0.3% forecast and accelerating from the previous 0.4%. The Y/Y rose by 2.9%, down from the prior 3.0% but above the 2.6% forecast. Core metrics surged by 0.8% M/M, exceeding the 0.3% forecast and the prior 0.6%, while the Y/Y increased by 3.6%, up from the prior 3.3% and the 3.0% forecast. Despite the strong core metrics, inflation concerns did not reignite, possibly due to softer PCE components within the report. Portfolio management and domestic air passenger transport fees decreased, while in healthcare, physician care costs increased, but other costs were little changed or decreased, with hospital outpatient care declining by 0.86% from the prior 0.02%. Pantheon Macroeconomics noted that the large upside was driven by a 2.5% increase in trade services prices, reversing the squeeze in H2 of 2025. They estimate that PPI and CPI data indicate the Core PCE deflator rose 0.27% in January and 2.9% Y/Y from 3.0% in December. Pantheon expects inflation to remain broadly unchanged over the next four months and anticipates a sharp drop in core PCE from June, ending the year slightly above the 2% target, supporting the case for looser policy.

FIXED INCOME

T-NOTE FUTURES (H6) SETTLED 14 TICKS HIGHER AT 113-27+

- T-notes rallied due to geopolitical risk and corporate credit risk concerns.

- At settlement: 2-year -5.3bps at 3.379%, 3-year −6.2bps at 3.382%, 5-year 5.3bps at 3.512%, 7-year −5bps at 3.719%, 10-year −4.2bps at 3.962%, 20-year −2.9bps at 4.571%, 30-year −2.4ps at 4.634%.

THE DAY:

- T-notes fluctuated overnight before rising throughout the European morning and the US session. The upside was driven by geopolitical tensions related to potential US action against Iran. Oman and Iran reported positive talks, but the US remained silent. Trump stated he has not decided on Iran and is dissatisfied with their negotiation methods. Embassies are being evacuated in the Middle East, increasing fears of a potential strike, although nothing is confirmed. Private credit fears persisted, with financials declining after the MFS collapse exposed several US PE firms and banks, including Wells Fargo, Apollo, and Jefferies. These concerns may be prompting a shift from corporate credit to safer government debt, supporting US T-notes. The PPI report was strong, driven by a jump in trade price services, while PCE components were less concerning. Pantheon Macroeconomics expects the Core PCE deflator at 0.3%, with the Y/Y at 2.9%, down from 3.0% in December.

SUPPLY

Bills

- The US will sell USD 77bln of 26-week bills and USD 89bln of 13-week bills on March 2nd and USD 90bln on March 3rd, all settling on March 5th.

Notes

STIRS/OPERATIONS

- Market Implied Fed Rate Cut Pricing: March 0bps, April 5.2bps, June 15.1bps, December 61.2bps.

- NY Fed RRP op demand at USD 16.32bln across 10 counterparties.

- SOFR at 3.67%, volumes at USD 3.262tln on February 26th.

- EFFR at 3.64%, volumes at USD 108bln on February 26th.

CRUDE

WTI (J6) SETTLED USD 1.82 HIGHER AT 67.02/BBL; BRENT (K6) SETTLED USD 2.03 HIGHER AT 72.87/BBL

- Crude oil prices increased due to ongoing concerns about escalating tensions between Iran and the US.

- Negotiations concluded without a deal, but both sides agreed to continue technical talks. Mediators cited “unprecedented openness” and narrowing gaps on nuclear limits and sanctions relief, though key sticking points remain. Trump stated he has not decided on Iran and is dissatisfied with their negotiation methods, but said there will be additional talks. He reiterated his desire for a deal and preventing Iran from acquiring nuclear weapons, and when asked about using military force in Iran, said he doesn't want to, but sometimes you have to. The lack of agreement and geopolitical uncertainty supported crude prices as some anticipate potential US action this weekend. Polymarket estimates a 26% chance of the US striking Iran by March 2nd. The weekly Baker Hughes rig count showed oil rigs down 2 to 407, natural gas rigs up 1 to 134, and the total down 1 at 550. WTI traded between USD 64.85-67.83/bbl and Brent between USD 70.42-73.54/bbl.

EQUITIES

CLOSES: SPX -0.43% at 6,879, NDX -0.30% at 24,960, DJI -1.05% at 48,977, RUT -1.68% at 2,632

SECTORS:

- Technology -2.17%, Financials -1.99%, Consumer Discretionary +0.03%, Industrials +0.23%, Real Estate +0.50%, Materials +0.80%, Utilities +1.07%, Communication Services +1.44%, Consumer Staples +1.51%, Energy +1.68%, Health +1.77%.

EUROPEAN CLOSES: Euro Stoxx 50 -0.51% at 6,130, Dax 40 +0.09% at 25,312, FTSE 100 +0.59% at 10,911, CAC 40 -0.47% at 8,581, FTSE MIB -0.46% at 47,210, IBEX 35 -0.73% at 18,361, PSI +0.09% at 9,276, SMI +0.94% at 14,045, AEX +0.45% at 1,027

STOCK SPECIFICS:

- Meta (META): Agreed to a multi-year deal worth billions of dollars to rent Google’s tensor processing units; Separately, last week, META scrapped its most advanced internally developed AI training chip

- Block (XYZ): Reduced its workforce by >40% due to a strategic shift towards AI and raised FY guidance.

- Dell (DELL): Reported strong Q4 results and guidance, driven by increased AI server demand and a growing backlog.

- Netflix (NFLX) declined to match Paramount Skydance's (PSKY) revised $31/shr all-cash offer for Warner Bros. Discovery (WBD), withdrawing from its previous $27.75/shr agreement.

- Intuit (INTU): Reported profit and revenue above expectations but issued a disappointing outlook.

- Zscaler (ZS): Guidance disappointed investor expectations.

- CoreWeave (CRWV): Reported a deeper loss per share than expected with weak next quarter revenue guidance.

- Flutter (FLUT): Revenue was light with an underwhelming FY outlook.

- Duolingo (DUOL): Reported weak quarterly numbers and guidance amid a strategic shift towards faster user growth that will weigh on bookings growth and profitability.

- Hunterbrook Research is short on Hercules Capital (HTGC).

- Caesars (CZR) says early talks focus on select assets, not full sale

FX

- The USD was mostly weaker against major currencies as a strong PPI report was overshadowed by a decline in US yields amid a flight to safety due to credit concerns, although the USD failed to capitalize on its typical safe-haven status given the increased bets in 2026 rate cuts. The Financials ETF XLF, initially resilient to credit concerns stemming from the UK lender MFS's collapse, declined alongside a further increase in credit spreads. Geopolitical concerns remain elevated ahead of the weekend, with Trump's remarks doing little to alleviate these fears. The PPI report was strong on both headline and core measures, with the Core M/M printing 0.8% in January, above the expected 0.3%, although components that feed into PCE showed little concern.

- The CHF led G10 gains, supported by risk aversion and higher gold prices, while the GBP lagged, unaffected by the Labour Party's loss in the Gorton & Denton by-election. USD/CHF traded around 0.7680, down from last Friday's close of 0.7772, while EUR/CHF hit new yearly lows of 0.9061. EUR/USD initially moved higher above 1.1800 on stronger-than-expected French and Spanish inflation, but the move faded after weaker-than-expected German State CPI data suggested a softer national print ahead.

- The JPY was marginally stronger against the USD, although upside may have been limited by recent nominations for the BoJ board, which are seen as indicating looser short-term policy. Tokyo CPI core inflation slipped below the BoJ’s target but was 1.8% Y/Y, above the forecasted 1.7%.

- USD/CNH weakened following the PBoC's decision to cut the FX Risk Reserve Ratio for forward FX sales to 0% from 20%, effective March 2nd, to promote FX market development and support corporate exchange rate risk management. USD/CNH reached highs of 6.8699 but later trimmed to 6.8590, still above the 6.8400 level seen prior to the PBoC announcement.